I will let the US Treasury Department explain:

Series I savings bonds protect you from inflation. With an I bond, you earn both a fixed rate of interest and a rate that changes with inflation. Twice a year, we set the inflation rate for the next 6 months.

https://www.treasurydirect.gov/savings-bonds/i-bonds/

These are savings bonds issued by the US government with rates that are tied to inflation. Since inflation has been crazy recently, the current rate is 9.62%. This is well above any other “riskless” investment, such as bank CD’s and other Treasury bills/notes/bonds. The only downside is that you must hold the bond for at least 12 months, and if you cash out before five years, you lose the last three months of interest. The bonds mature in 30 years, which means no more interest. Also, you can only purchase $10,000 of I bonds annually, and the interest rate is reset every six months. Confusing, huh?

My mom and I purchased $10,000 each back in April to capture a 7.12% rate, knowing that the next rate will be 9.62%. The estimated rate starting November 2022 is 6.48%. High-yield savings accounts are paying between 2.0% to 2.5% so I bonds are a good deal. If the rate stays high, then keep holding the bond. Once inflation drops and the combined interest rate falls below savings accounts, then cash in the bond.

To get more bonds at the 9.62% rate, you can also gift I bonds to other people. I did this with my mom as we each purchased $10,000 gift bonds for each other. The bonds have the same interest and date restrictions as a regular bond but is held in limbo until the recipient accepts the bond. The recipient must still adhere to the $10,000 limit each year. So next April, when we know the next I bond rate, if it is higher than 9.62%, then we will purchase a new bond. If not, then we can accept the gift bond from this year. More confusion.

==========

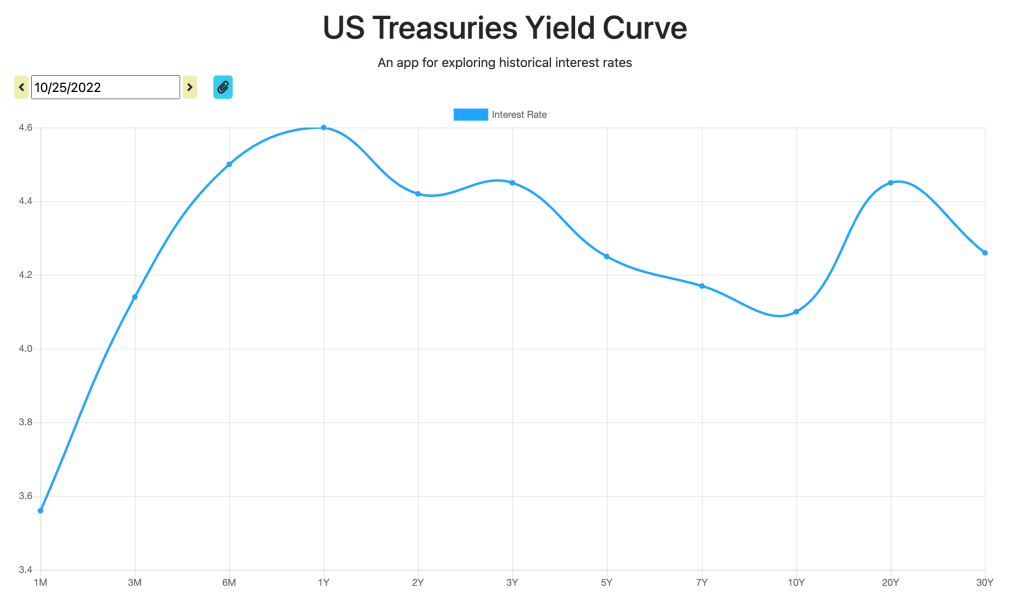

We have also been purchasing 4-week treasury bills. This is like buying a one-month non-cancellable CD. Last week’s auction resulted in a 3.487% rate. All the short-term T-bill rates will likely continue to increase so this will remain a viable investment for a few more months. If I was more tolerant of duration risk, I would buy some one-year T-bills as it has the highest returns currently.