Since I returned to work early February after heart surgery, I’ve been only going in to the office three days a week due to dialysis. With the ramp up in COVID-19 hysteria, I think I need to talk to my boss about working from home more often, maybe only go in to the office once a week for meetings. The issue is that both me and my parents are in the high risk group, which has a much higher mortality rate. From cdc.gov:

In the past, my primary doctor and the dialysis clinic have been pretty adamant about me getting the flu shot each year. They said even regular influenza is dangerous for me being diabetic and on dialysis. This current pandemic is definitely a lot worse. I’ve been using up a lot of vacation time to cover my Tuesday/Thursday absences. Maybe it’s time to switch to 3/4 time and the corresponding 25% reduction in salary.

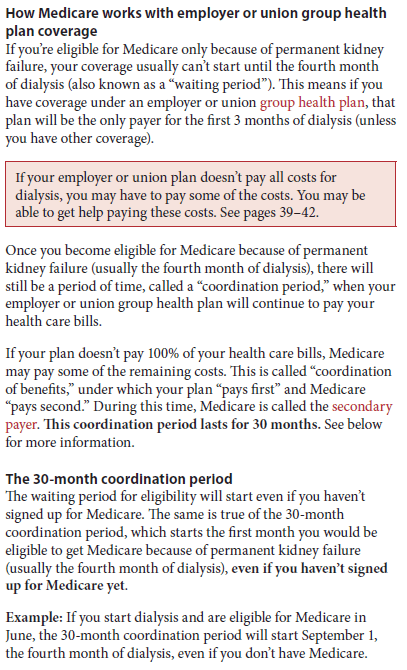

It’s getting serious now. My insurance just rejected my February dialysis bill for ~$33k. I still can’t get through to Medicare’s benefit coordination center; the wait time was too long last time so I need to try again tomorrow. However, I found a document on Medicare’s website that clearly states that I need to wait 3-months before beginning Medicare, and the 30-month benefits coordination starts after that date. That is why all the info I’ve received from my dialysis clinic mention the coordination period as 33-months. Now all I have to do is get my work insurance to agree and reprocess all the rejected claims.

I’m so frustrated with all this. I called our work insurance service provider again today and spoke to the claim supervisor. It turned out he has been out sick so he never got back to me. Anyway, their conclusion is that after 30-months of dialysis, Medicare becomes the primary insurance for all claims. Therefore, I need to have all my providers bill Medicare first, then any remaining amount will be paid by my work insurance. The problem is that Medicare starts three months after the first dialysis date of July 5, 2017, so by rejecting claims after January 5, 2020, my insurance is off by three months. The rules are so confusing that each time I call my insurance or Medicare, the answer seems to change. I’m now getting invoices for this failure of benefits coordination.

DENIED!

Because of this confusion, I’ve stopped seeing my therapist and acupuncturist. I also have several upcoming appointments to see the cardiologist, primary care physician, endocrinologist, and others. I feel like I need to postpone those appointments until the insurance situation is cleared up. My work insurance also started rejecting my cardiac rehab claims so I’m not sure how to continue there since the hospital doesn’t seem to want to bill Medicare on my behalf.

Since I got no sleep this morning at all, I am super tired right now. I’ve already fallen asleep at my work desk for 20 minutes. Luckily I’m in the corner cubicle; if I sit low, no one can see me and unless they are looking for me specifically, there’s no reason to walk back here.

Not me… but very close

It’s about 5:40 pm. I think I’m too tired to do any more work so I’m going to go home. I’ll try to get a cup of coffee on the way out so I can have something to keep me awake on the drive home since it will be >1 hour to drive home. When will companies tell workers to telecommute in Los Angeles? Either I will get to work from home or there will be a lot less traffic.

Less red but still a lot of traffic and one hour+ to drive home from work

I’m not sure what to do about my work insurance screw up. My therapist basically suggested we stop meeting until the payment issue is resolved. I don’t think she has received any rejected claims back yet but we’re stopping anyway. There could be as many as four rejected claims for my therapist so that’s an extra $400 I would have to front and maybe get reimbursed later.

This is happening to claims from the acupuncturist as well. I’m still going tonight but will probably have to stop. There are a lot more potential claims to reject since I’ve been going twice a week. Also, Medicare does not cover acupuncture nor elective therapy so even if Medicare was my primary insurance, my work insurance would still have to pay these claims. I wish they would at least stop processing claims while researching the case instead of going ahead and rejecting them and causing me a lot more work later on.

I also skipped cardiac rehab today. It’s been over a week since I went. I missed a couple due to feeling like crap after dialysis, one due to an early work event, and one due to my tooth hurting from a dentist appointment. When I walked out of dialysis today, my legs felt weak so I didn’t want to walk another 30 minutes on the treadmill. I need to get lots of sleep tonight so I can go in tomorrow morning. I can still meet UCLA’s April deadline if I don’t miss too many sessions from now on.

I just checked my work health insurance activity and they rejected all sorts of claims, even after my phone calls and emails clarifying that Medicare is secondary insurance, not primary. I called their customer support and it seems that they are still researching my case. They still think Medicare pays primary until 30 months or something. During our last conversation, a supervisor clearly said they were going to make a note about Medicare being secondary insurance in my files, and reprocess all messed up claims. I guess not. Now there are even more messed up claims, some for thousands of dollars, that I have to deal with with time I don’t have.

It’s been about a month since I returned to work. I’m only going into the office three days a week due to my hemodialysis sessions on Tuesdays and Thursdays. I still feel out of sync however. I’m not making much progress learning the new system we put in while I was on leave, and I can’t focus on other projects. I’ve been letting my junior analyst take care of all the regular tasks but she is out this entire week so I have to get some reports out. My boss is also expecting a 90 day plan; I don’t have any ideas yet.

At home, it’s also weird. I spend four out of seven days at home so it doesn’t feel like I’m back to work. I still lose track what day of the week it is sometimes.

I called Medicare today with questions regarding coordination of benefits when I still have my work insurance. The person on the phone was really nice but the call took awhile since she had to look up a lot of info. I guess it’s not a common topic.

She confirmed that as long as I have my work insurance, Medicare will pay as secondary insurance, except for dialysis after 30 months, and the kidney transplant. I asked about previous claims where I paid a co-pay and was told that I can file a claim. However, if the provider charged more than the Medicare rate, and most do for private insurance, Medicare will calculate their responsibility with the lower rate. I’m still unclear what that means. If my doctors bills my insurance $200 and they paid $160 since my co-pay was $40, how much will Medicare reimburse me? If the Medicare rate is $100, will they pay up to $80 (80% of the initial claim at the lower rate), or pro-rate my co-pay and only reimburse me $20? We decided over the phone that I should just file the claim for $40 and see what happens. I also didn’t get any statements from my doctors so I’ll need to go back to all of them for more info in order to file the claims. Medicare does pay for cardiac rehab so that’s a lot of co-pay to get back for the entire program.

I also got the first statement from my dialysis clinic. The insurance amount was close to $30k. My work insurance only pays 85% but since I also have an out-of-pocket maximum each year, my portion comes out to ~$3,000. I’m thinking Medicare should pay that but their dialysis reimbursement rate is much lower, probably like $3,600. So will Medicare pay only 80% of that or $2,880? Also, if Medicare pays some of the bill, will my insurance count that when calculating my out-of-pocket maximum? Otherwise I’ve hit my max and my work insurance will pay 100% from now on. Super confusing.

Crap! There were five claims (so far) that my work health insurance screwed up. When I called them, I thought there was only one but after going through all the claim activity online, there were four more where my work plan paid as if they were the secondary insurance. I sent them a secure message on their platform with all five claim statements. I hope they review and repay in a timely manner so I don’t have to answer all sorts of calls from my doctors. Sigh…

I still have to call Medicare to figure out what to do with all my co-pays. I figure I must have paid >$350 in co-pays excluding acupuncture and therapy. Not sure if those two things are covered. I called Medicare once before and they were pretty helpful so maybe this won’t hurt too much.

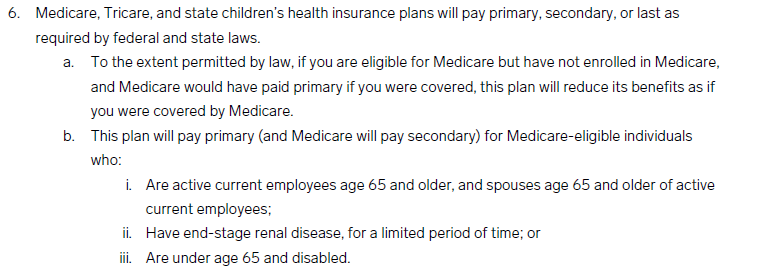

I talked to our benefits department and they found an 85-page plan detail document from 2017 that clearly states if I qualified for Medicare because of ESRD, our insurance plan would be primary and Medicare would be secondary. This is contrary to the last claim details I received. Our benefits coordinator requested a callback from a supervisor from our insurance and he verified that our plan should be primary. He also said he would ask his team to reprocess my claims again to make sure they were paid out correctly. Yay! I was afraid I had to mediate between insurance plans if both thought they were secondary insurance.

Pretty clear, no?

Like my sister, our benefits coordinator said this coordination of benefits when you have multiple insurance coverage is the most complicated topic in health insurance. No one wants to be the primary coverage insurance since they usually paid 80%-85% of the claim. I avoided getting Medicare because of this coordination mess, and only got it because my work insurance will stop paying for dialysis soon.

Several years ago, my benefits coordinator at work told me about some supplemental insurance programs that we were offering for extra cost. The programs were underwritten by Allstate Benefits and included Critical Illness Insurance and Hospital Indemnity Insurance. I signed up for both since I was already at stage 5 of CKD (chronic kidney disease). For Critical Illness Insurance, I enrolled in Plan 4 which costs about $50 each pay period and pays $50k per illness. That same year, I started hemodialysis in July but never filed a claim with the insurance. With the recent heart bypass surgery, I now have two claims to file.

For some reason, they only pay out 25% for CABG surgery. Maybe it’s not as serious as ESRD (ha!). Also, if you have a second critical illness event of the same type, they will pay again. I don’t know how they would treat ESRD since I went from hemodialysis to peritoneal dialysis and back again. Probably counts as one illness event since I never stopped dialysis. My benefits coordinator said she will help me fill out the claim forms. For sure I can claim both the ESRD and CABG items for $50,000 + $12,500. If I have the transplant this year, then it’s another $50,000 for a major organ transplant. Not bad for $1,300/year in premiums.

The other insurance for hospital indemnity doesn’t pay that well. It pays $1,500 for the first day, then up to 10 additional days at $150/day. You can also only make one claim per year. I don’t know if they will count my CABG surgery as two claims: critical illness plus hospital stay. You really can’t have the surgery without staying in the hospital. If they count it as a separate claim, then it’s $1,500 + $150 x 9 days = $2,850. I also stayed in the hospital for a few days back in 2018 for a foot biopsy. Looking at old medical claim forms, it appears to be three days in May 2018 so maybe another $1,500 + $150 x 2 days = $1,800. I hope Allstate doesn’t drop our insurance coverage because of me.

If any of my claims are paid, I told my benefits coordinator that I’d buy her a nice steak dinner.

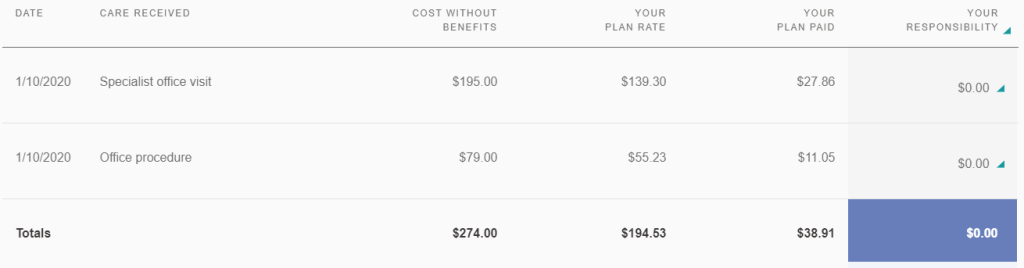

The fun starts now! Back on January 10th, I went to see a podiatrist for a check up since I’m diabetic and have peripheral neuropathy. Since the podiatrist was a specialist, I paid my $40 co-pay and thought everything was fine. Well, the podiatrist office finally filed the insurance claim, and I got the following statement of benefit from my work insurance.

The podiatrist office billed $274.00 for my visit but the negotiated rate for Blue Shield is $194.53. My insurance then determined that since I have Medicare starting 1/1/2020, they are the primary insurance, and should cover 80% or $155.62. Therefore, my work insurance only needs to cover the remaining 20% or $38.91. On my call with my work insurance yesterday, they said I need to give all my providers a copy of my Medicare card so they can bill Medicare. For this claim, I should get my $40 back once Medicare pays. I had a lot of doctor appointments in January. Since none of the claims have been processed, I will need to do this with 5-6 providers and lots of claims.

I see some potential problems with this. First, once I pay my co-pay, it’s very hard to get that money back. I have to follow up on each claim to see if and how much Medicare pays, and harass the doctor’s office for refund. Also, who determines which insurance is primary? What if Medicare decides they are secondary and my work insurance should pay 85% first? Also, for the claim above, the plan rate was less than what the podiatrist billed. What is the Medicare plan rate? I think it’s often less than private insurance reimbursement rate. So what if Medicare’s rate is only $100 and they pay 80% or $80? What happens then? What if the medical provider does not accept Medicare in the first place? Sometimes I think having a single health insurance payer, like they do in Canada, is much easier on the consumer. Doctors and hospitals will probably lose out though since reimbursement rates will definitely be lower.

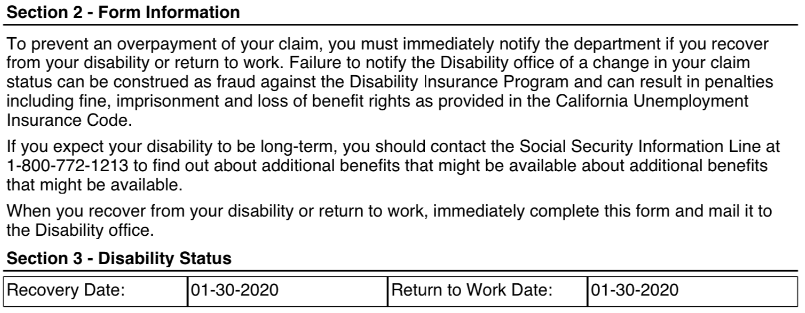

The California EDD must have processed my return to work form since they sent me another check for 1/28 and 1/29. Looking at the check stub, I realized I screwed up the dates again. I must have misread the form and put in the wrong dates. There is a field for recovery date and another one for return to work date. Like an idiot, I put down 1/30 for both instead of 1/31 for return to work date. I was actually still out on leave on 1/30, which means no pay from work. The difference for one day of disability is $178.66 before taxes. To change my return to work date and get that money will require a doctor to fill out a four page form. $180 can buy a nice meal but I think I’m going to forget it. It’s going to look very stupid filling out another disability justification form for just one day when I’ve been ok for the past few weeks.

At least now I know to read the damn forms more carefully. I will need to to all this again in a few months if the live donor kidney transplant goes through. The recovery for that is also around three months.

I created an account on DaVita’s website even though I’m not a patient. They have a lot of information on kidney failure, dialysis, and diet. I was specifically interested in their Diet Helper™ which has a lot of recipes and nutritional information.

Today, I received an email from DaVita pointing to the Employment page of their website. Basically, the email says dialysis patients should keep working if possible because it keeps you healthier and happier. My dialysis social worker says this too. It’s better for your mental health if you can continue working instead of quitting and getting Social Security disability.

Working and Dialysis

There could be another reason DaVita want their patients to keep working. 90% of their patients have Medicare as their primary insurance. Medicare reimbursement is pretty low so all their profit comes from the 10% with private insurance. I know I pay about 10x the Medicare rate to St. Joseph Hospital for dialysis in the past. Once I switch to Medicare as the primary insurance, that reimbursement amount will be a lot less.

Having not worked for three months and being on hemodialysis for most of that time, I would agree that working is good for your mental health. I was going crazy sitting at home all the time. Often I lost track of what day of the week it was since I didn’t have the weekly work schedule to keep track of time. Also a lot of my non-family relationships are with co-workers and not having regular contact for three months was very isolating. Of course, work has its own set of issues, namely stress and fatigue, but if you can work, you should try to work as long as possible.

I’m still writing down blood pressure readings during dialysis, trying to figure out the pattern and how to minimize the fluctuation. Here are some readings from today:

Time

Systolic

Diastolic

Pulse

Notes

8:50 am

127

73

65

Standing

8:55 am

137

78

63

Sitting/legs up

9:07 am

148

83

63

Sitting/legs up

9:38 am

131

77

63

Sitting/legs up

11:08 am

178

88

65

Sitting/legs up

11:38 am

156

88

65

Sitting/legs down

12:45 pm

171

Sitting/legs down

1:00 pm

131

Standing

I can’t remember what I was doing between 9:30 am and 11:00 am but I missed several readings. My nephrologist agrees that likely the Metoprolol is being dialyzed out of my bloodstream during dialysis but she doesn’t want to prescribe more drugs yet. She did say the both the Metoprolol (beta blocker) and Olmesartan (ARB) are good for heart disease patients. NIFEdipine, even though it works great on me, doesn’t have any heart protection properties.

I handed a copy of my Medicare card to the front counter person. She said she will give it to my dialysis social worker. I hope they know how to coordinate billing since Medicare is supposed to pick up whatever my insurance does not pay. That is probably ~$3,000 since I am responsible for 85% of dialysis costs until I hit my out-of-pocket max. I still don’t know if Medicare covers my work insurance co-pays because I paid $280 already just for acupuncture co-pays.

One of life’s greatest mysteries is healthcare pricing in the US. You have a list price that patients are supposedly charged if they do not have insurance, you have an insurance negotiated price, then there is the co-pay that the patient is responsible for. I tried looking at my dialysis and emergency room statements and I can’t figure them out. BTW, I have a MBA degree in Finance.

Provider website

For acupuncture, the provider’s website says they charge $90 for the first visit (consultation), then $60 for subsequent visits. It doesn’t say whether that’s for acupuncture or chiropractor so I assume it’s both. My co-pay for each session is $40, so I thought my insurance is paid $50 for the first session, then $20 for subsequent visits. Nope.

Insurance statement for second acupuncture session

For the first visit, the provider billed $290, which has an insurance price of $125. Out of that amount, my insurance paid $85 and I paid $40. For subsequent visits, they billed $180, which became $75. My insurance paid $35 and I still paid $40. Why aren’t they billing $90 and $60 per their website? My insurance will only pay for 30 sessions. Does that mean they make less money if they bill me directly without insurance?

I’m at work right now… blogging. So today was my first day back to work. It’s weird because it feels like I’ve been gone forever, but everything is still the same. I met with my new staff and old teammates to get caught up. While I was gone, my work email account went over quota so I could not send any emails. It took me several hours to go through three months of unread emails and delete enough stuff so I’m under quota again. Security also did not turn on my badge so I could not get in the building initially. Unlike last time, a quick phone call to HR to confirm my leave status and I was back to normal.

We have something similar at all our building entrances

Physically I felt fine. The drive was not too bad and none of the surgery sites hurt too much. Since I have dialysis tomorrow, I have to take a day off and continue work tasks Friday. I’m probably eating and drinking more since there are several cafeterias and free fountain drinks at work so getting food is very convenient. Got to be careful not to gain back all the weight I lost during recovery.

First thing I have to do is put my dialysis times on my calendar so no one tries to schedule a meeting during those times.

I got another disability check from the EDD today. It’s payment for 1/14/2020 through 1/27/2020. My cardiologist had told them that I would be out on disability until 2/14/2020 but I’m actually ending my leave on 1/30/2020. I believe it’s a big no no to get state disability pay if you are getting paid from your employer. I went online and filled out a DE2587 (Recovery or Return to Work Certification) form so hopefully they will process the form and just pay me for a few more days instead of two more weeks.

Crap! I just noticed it said to mail in the form. Of course it does not provide an address. Why would they want me to mail a form that was generated online? Is this the best technology the state of California can come up with? I’m glad that I was able to get some disability payments while I was on medical leave but the less I have to deal with the EDD, the better.

Also, I completed the form on my iPad and could not figure out how to save the PDF. The above is a snip of a screenshot from the iPad. In my attempt to save or export the PDF, the message this from came from was deleted. Of course there is no other way to get to the form other than the Inbox message. At least I got a screenshot.

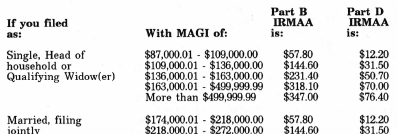

I got my Medicare card in the mail. I already have my Medicare number from a different letter but having the card seems more legit. I also got a notice of Medicare Part B premiums. I thought based on my last tax return, my premium would be $433.40/month. I guess I had the wrong lookup chart. The letter says my premium will be $318.10/month, which is $115.30/month less. That’s a lot of breakfast burritos.

What’s weird is I looked up the Medicare website and they also have a different rate table than my original post and the letter I received.

Here it looks like my premium will be $462.70/month. However, the letter had these set of numbers:

At first I thought the premiums table at the website was adding Part B and Part D premiums but the math doesn’t work out either. With the cost of dialysis so high, I’ll pay whatever they bill me. Again, I don’t know who pays for the kidney transplant if it happens this summer. Also, I don’t have Medicare Part D. Does Medicare still cover post-transplant medication?

After I had my emergency heart bypass surgery, I was discussing the future with someone from my church small group. His comment was that my previous life was over and I need to think about how to live my second life. For now, I’m going to go back to work but really think about what to do with the rest of my life. 25 years in finance is a long time.

One idea is to find a job closer to home, but several levels below my current position. I’ve been in a director level position for the past 8+ years, which means managing staff that manages other employees. A lot of my time is spent mentoring instead of getting tasks done. Maybe I can take an analyst position nearby and take it easy, but for a lot less pay.

Taipei skyline

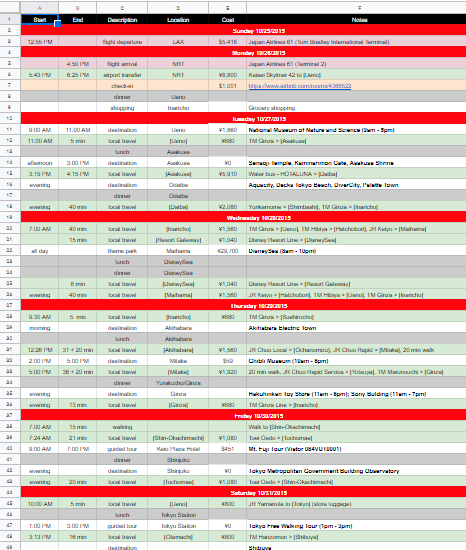

Another idea is to find another career in an entirely different field. I really enjoy putting trips together. On our 2015 family trip to Japan and Taiwan, I spent about three months researching and organizing a detailed itinerary that even included train schedules and restaurant listings. I managed to get it down to two pages and we carried it with us all trip. However, usually when you start a new career at the bottom, you have to work really hard. I don’t mind working hard but I don’t really have a career goal at this point. Also, how do you start with no experience? Do I need to take classes in school again?

First half of our Asia trip itinerary

I looked at tour operator sites like Abercrombie & Kent and it seems like there are pretty healthy profit margins. Closer to home, I found this tour at Kensington Tours that charges ~$5k/person for six days in Southern California. Assuming they will operate the tour with just two guests, that’s a budget of ~$10k. Let’s break down the itinerary:

Accommodations at Hotel Indigo: about $265/night for King Skyline View room

Day 1: pick up guests at airport

Day 2: 4 hour tour of Los Angeles: the only place that looks like it needs tickets is La Brea Tar Pits ($22/person); not sure if lunch at The Ivy is included; parking at Griffith Observatory is ~$10/hour

Day 3: 9.5 hour trip to Santa Barbara: visits to a bunch of public places so if there are tickets and parking, it’s probably not too expensive; again, not sure if lunch is included; winery tours are probably free; private wine tasting seems to be $35/person

Day 4: 6 hour drive down to San Diego: all the stops in LA are public locations and free

Day 5: 4 hour tour of San Diego: only place that costs money is visiting the USS Midway Museum ($26/person)

Day 6: drop off at airport

If we pay the tour guide $30/hour and we include 10 hours/day, then it’s ~$2k for labor. Accommodations for five nights is ~$2k, and everything else is probably <$1k (transportation, parking, admissions, maybe food). That leaves ~$5k of profit for only two guests (50% margins!). If you have two more guests, just rent a minivan and get another hotel room. The profit margin is even higher with more guests. Of course there are risks, such as sitting around having no customers, but it sure beats working fast food. Maybe even better than working as a finance director.